By Javier Blas

Can the global economy weather oil trading at $100-a-barrel next year? Because a triple-digit price tag wouldn’t just mean elevated energy prices — it would also turbocharge the dollar. The combination of expensive barrels and a rampaging greenback could make crude a wrecking ball in 2024 that keeps inflation high enough to destroy growth around the world.

The more oil soars, the pricier the dollar is likely to be, creating a pernicious feedback loop. The longer the cycle continues, the more pain will be felt.The link between petroleum and the greenback is American inflation.

As US retail gasoline and diesel prices climb, they could exacerbate domestic inflationary pressures in other sectors, convincing the Federal Reserve to keep interest rates higher — or even higher — for longer.

The world’s oil central banker, Saudi Energy Minister Prince Abdulaziz bin Salman, and the dollar central banker, Jerome Powell of the Federal Reserve, are working hand-in-hand in some ways. The result could be a slowdown in oil demand growth in 2024.

Japan is perhaps the best example of the oil-and-currency cocktail. The yen is hovering at its weakest exchange rate against the greenback in nearly 35 years, turning petroleum refined products into a small luxury. Last month, the Japanese government was forced to extend fossil-fuel subsidies until the end of the year after the nationwide retail gasoline price jumped to a record high of 186.5 yen ($1.24) a liter, surpassing the peak set in 2008.

For now, the countries most affected by the toxic oil and dollar-strength cocktail aren’t the global centers of energy demand growth. Instead of China and Brazil, think about Kenya and Argentina. Still, on the margins, they matter.Oil traders currently say there’s little sign that global demand is taking a big hit. True, petroleum consumption has hit the brakes in West Africa, but the biggest reason is the removal of subsidies in Nigeria.

Elsewhere, demand remains healthy.But if prices remain close to their present levels, the ache would slowly be felt in the world’s engines of demand, notably India. As the rupee has been losing value steadily against the dollar, New Delhi is finding that, in local currency, oil is more costly than when it hit $150 a barrel in 2008.

India has already told petroleum-producing countries that prices are too high, Oil Secretary Pankaj Jain said earlier this week. “High prices lead to demand destruction,” he commented. Another unacknowledged problem for emerging markets like India and China: The benefit of their non-aligned oil policy is ending. For most of 2022 and early 2023, New Delhi and Beijing have had access to cheaper crude by buying heavily discounted barrels from Iran, Venezuela and, above all, Russia.

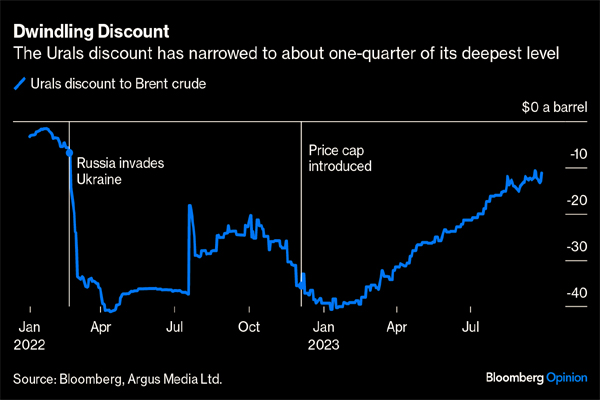

By refusing to take sides in the Ukrainian war, India and China have extracted an economic rent. Since then, though, the discounts that Tehran, Caracas and Moscow offered have narrowed considerably. Russian flagship Urals crude, for example, sold at one point in early 2023 at nearly $40 a barrel below Brent, the global benchmark. Now, Urals is selling at about $10 a barrel under Brent.

With the post-pandemic rebound in global fuel use running out of steam, the International Energy Agency anticipates that world oil demand would slow down in 2024 to about an extra one million barrels a day, down from 2.2 million barrels a day in 2023.The expected increase in oil demand growth next year is nonetheless within the historical average for the pre-Covid-19 era.

If demand increases by one million barrels a day, as the IEA is expecting now, Saudi Arabia’s Prince Abdulaziz will remain in command of the oil market. The increase would be enough to absorb extra production from the likes of Brazil, Canada, Guyana and the US in 2024, plus OPEC+ nations eager to increase output, particularly the United Arab Emirates, but perhaps also Iraq.

But any growth slowdown could overwhelm the market, forcing Riyadh to keep its unilateral output cuts much longer than expected, or face lower prices.In commodity markets, high prices are the cure for high prices. Saudi Arabia and the Fed are giving the global economy plenty of medicine to treat the ailment. In the process, they may kill the patient. Beware.

____________________________________________________________________

Javier Blas is a Bloomberg Opinion columnist covering energy and commodities. He previously was commodities editor at the Financial Times and is the coauthor of “The World for Sale: Money, Power, and the Traders Who Barter the Earth’s Resources.” @JavierBlas. Energiesnet.com does not necessarily share these views.

Editor’s Note: This article was originally published by Bloomberg Opinion, on October 4, 2023. All comments posted and published on EnergiesNet.com, do not reflect either for or against the opinion expressed in the comment as an endorsement of EnergiesNet.com or Petroleumworld.

Use Notice: This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in our efforts to advance understanding of issues of environmental and humanitarian significance. We believe this constitutes a ‘fair use’ of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U.S.C. Section 107. For more information go to: http://www.law.cornell.edu/uscode/17/107.shtml.

EnergiesNet.com 10 05 2023