Thomas Washington, Robert Perkins and Sasha Fosss, Platts S&P Global

LONDON

EnergiesNet.com 11 17 2023

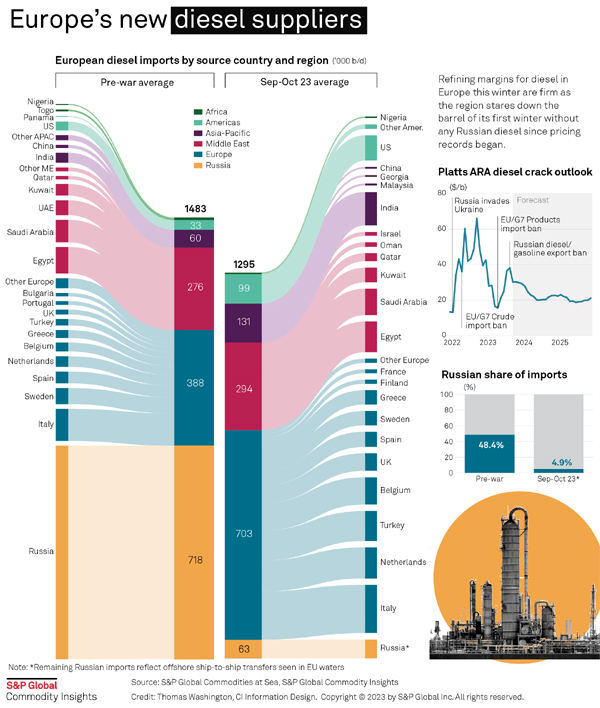

The outlook for diesel cracks in Europe this winter remains well above seasonal norms as the region stares down the barrel of its first winter without any Russian diesel imports since pricing records began.

The EU banned imports of Russian oil products effective Feb. 5 in response to Russia’s invasion of Ukraine, forcing the trade bloc to reconfigure its diesel-hungry trade flows.

Before the war, Europe was a major buyer of Russian diesel, importing some 780,000 b/d in February 2022. In October 2023 just 80,000 b/d of Russian diesel was seen in European waters, according to data from S&P Global Commodities at Sea, largely reflecting ship-to-ship transfers off the coast of Greece.

To fill the gap, Europe has turned to alternative sources such as the Middle East and the US Gulf Coast.

In February 2022 Saudi Arabia sent 72,000 b/d to Europe but in September 2023 supplied 137,000 b/d, falling to 109,000 b/d in October. The US loaded 43,000 b/d before the war and in September loaded 109,000 b/d, falling back to 43,000 b/d in October, according to CAS data.

Imports from India have also ballooned as Moscow’s biggest crude buyer exports more fuels made from discounted Russian crude.

However, questions surround the cold flow properties and the volumes available of alternative diesel to Russia’s, according to traders. Diesel sold into Europe over winter must still be able to flow at low temperatures before it becomes waxy, and while Russian diesel is refined to accommodate this, not all diesel performs as well in the cold.

Diesel cracks — the difference between the price of a barrel of crude and the diesel extracted from it — have been buoyant as a result. The crack spread for diesel in Northwest Europe in January 2022 was $13.33/b, against a five-year average until that point of $10.99/b ,according to data from analysts at S&P Global Commodity Insights.

Export ban effects

Regional diesel cracks have also been supported by Russia’s temporary ban on most diesel and gasoline exports, announced Sept. 21, in a bid to curb soaring domestic pump prices. Exports by pipeline have since resumed but seaborne barrels are still forbidden.

The Russian government is monitoring the situation with oil products and would consider easing the export ban in the event of a lack of domestic outlets as refinery output increases, Deputy Prime Minister Alexander Novak said.

Analysts at S&P Global expect diesel cracks in Europe to decline over the winter, but remain above $24/b through to March, more than double seasonal norms.

“ARA diesel cracks have eased from summer highs, but heating demand and low inventories in the Atlantic Basin will continue to drive cracks this winter,” Rebeka Foley, Senior Analyst, Oil Markets Pricing & Trade Flow at S&P Global, said.

European refiners are struggling to build inventories despite high diesel yields, with runs in Europe in the second and third quarters of this year below average levels. Backwardation in the M1-M2 curve has recently softened, implying less prompt tightness, but higher front-month prices continue to hurt storage economics and preclude stockbuilds, Foley said.

Distillate stocks in the Amsterdam-Rotterdam-Antwerp region amounted to 13.9 million barrels in the week of Oct. 19, well below the five-year average of around 18 million barrels, according to S&P Global data.

“We see these bullish fundamentals keeping ARA diesel cracks at around $30/b through end-year before gradually easing to around $25/b by March,” Foley said.

Promising alternative sources to Russia this winter include the US Gulf, following the commissioning of ExxonMobil’s Beaumont refinery expansion, and the Middle East as Kuwait’s Al-Zour plant approaches its nameplate capacity and as Oman’s Duqm continues to ramp up.

Further East, India could ship higher volumes to Europe but European traders will have to compete against those in Asia and while China could theoretically supply incremental barrels this looks unlikely since Beijing ruled out releasing extra product export quotas over the fourth quarter, implying Chinese diesel exports will continue to head to Asian destinations, Andrew Wilson, Head of Research and Consultancy Services at BRS Shipbrokers, told S&P Global.

All eyes are on cargoes from India and the Middle East to plug the gap in European supply, while US Gulf Coast exports fall amid a resurgence in domestic consumption, S&P Global analysts said.

spglobal.com 11 16 2023