- Citi forecasts about $100 billion in regional sales this year

- Issuers come to market as hopes for US rate cuts in 2023 fade

Esteban Duarte, Bloomberg News

SAO PAULO

EnergiesNet.com 07 17 2023

International bond sales out of Latin America are on the rise again as hopes for US rate cuts this year fade, leading companies and governments back to the capital markets.

Issuers from the private and public sector have raised more than $49 billion by selling bonds denominated in reserve and local currencies through July 13, according to data compiled by Bloomberg. That’s just $9 billion short of the $58 billion raised in all of 2022, the slowest year in terms of sales since 2008. For this year, bankers at Citigroup Inc. forecast close to $100 billion in international bond sales from the region, while BNP Paribas SA expects about $60 billion of such deals.

Central banks in the region started tightening their monetary policy ahead of their counterparts in the US and elsewhere, allowing for potential rate cuts. In the US, traders are pricing in another 25-basis points rate hike, which would bring the Federal Reserve’s benchmark rate to a target range between 5.25% and 5.5% — around 100 basis points higher than what market participants were forecasting in May for the end of the year, according to data compiled by Bloomberg.

“Some sovereigns still have some funding needs and might look to pre-fund next year’s budget given the constructive primary market tone,” said Anna Abadias, a vice president in BNP’s LatAm debt capital markets team. The bank expects highly ranked corporates and financial institutions to consider tapping the market “now that rates are expected to remain higher for longer,” she said.

Several deals could come to market in the second half of the year. Brazil hired Banco Itau BBA, JPMorgan Chase & Co. and Banco Santander Brasil SA to assist with the nation’s first-ever sustainable bond sale, a long-awaited transaction that’s expected to hit markets by the end of the year.

The Brazilian Treasury said Friday it would also monitor market conditions for possible issuances of traditional external debt. The Latin American nation may tap its 6% bond due in 2033, a person familiar with the matter said last month.

Banco Internacional, a Chilean commercial bank, recently conducted a series of video conferences ahead of a potential five-year benchmark transaction, denominated in dollars, people familiar with the matter said earlier this week. A press officer for the Santiago-based bank didn’t immediately respond to a request for a comment.

Chile and Paraguay, as well as oil majors Petroleo Brasileiro SA and Ecopetrol SA, were among the Latin American issuers that priced dollar-denominated transactions in June. Petrobras raised $1.25 billion with a 10-year bond that attracted an order book 3.4 times of the deal size, the company said in a July 3 statement. The company is monitoring the markets and weighing additional transactions that would reduce the cost of capital by canceling its most expensive debt ahead of time, Chief Financial Officer Sergio Caetano Leite said in an interview.

“The time had come to put our feet in the water and see what the temperature was,” he said. “The acceptance was good, which leads us to continue looking at the debt markets. Petrobras is back to the game.”

Latin American corporates are venturing back into the market, said Adrian Guzzoni, Latin America head of debt capital markets at Citi. The expectation is that the “market will continue to improve in terms of volumes” said Guzzoni. “When some of the corporates start coming, obviously lot many others follow suit.”

Another driver for new issues could be the need to refinance bank facilities that companies took on to avoid having to tap the bond markets during recent periods of market volatility, said Juan Fullaondo, head of Latin America and Caribbean debt capital markets at Bank of Nova Scotia.

Issuers are also registering investor demand for bond sales in local currencies. Uruguay, Chile, Peru and the Dominican Republic this year have priced local-currency debt in a format that makes easy to buy for domestic and international investors alike. These bonds can usually be settled by clearing houses widely used by international investors, including Euroclear.

“Seeing transactions in local currency with some international investors is a good sign in terms of openness in the market because those trades typically are done in healthy markets,” said Guzzoni.

Mexico will offer a sustainable bond maturing in May 2035 with an 8% coupon on July 20, the country’s central bank said Wednesday.

Read more: World-Beating Currency Rally Spurs Latin America Debt Sales

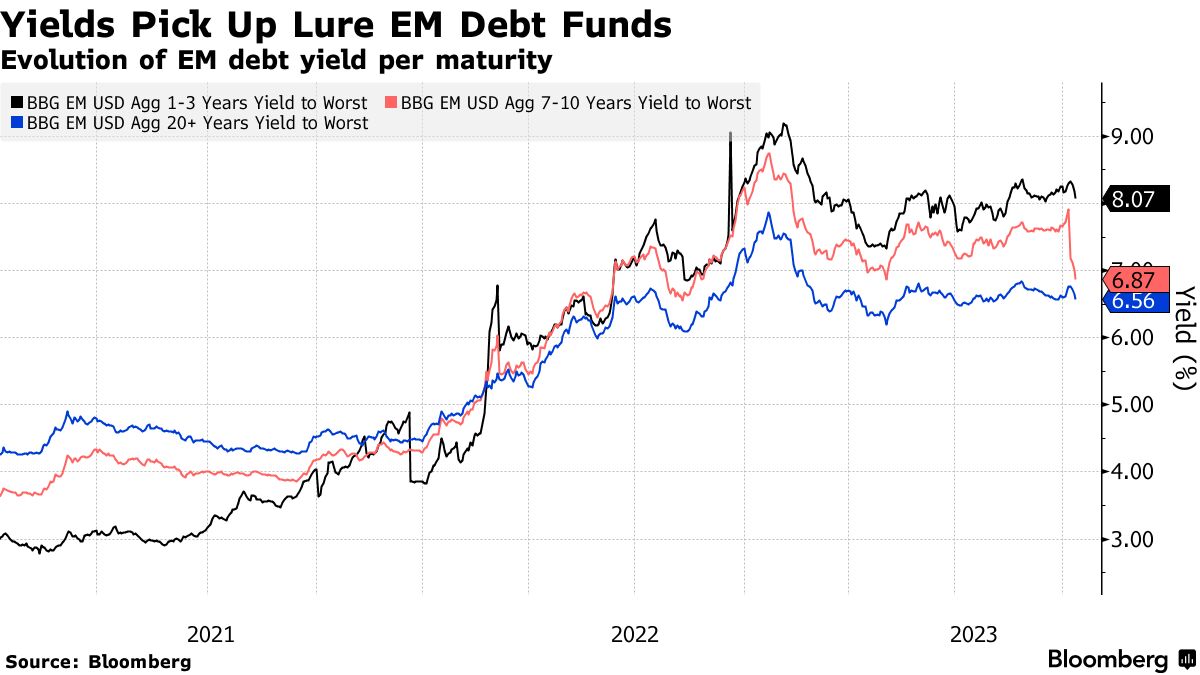

Emerging-market yields have stabilized in recent months, but remain at significantly higher levels than a year ago. That however isn’t deterring issuers. “Issuers are taking advantage of the constructive market tone to refinance upcoming maturities and extend their maturity profiles,” BNP’s Abadias said.

“While in many cases these exercises lead to more costly new debt, nobody can predict whether demand for longer-dated credit will be there next year,” Abadias said.

— With Mariana Durao, Michael O’Boyle, Maria Elena Vizcaino, and Andrea D Niper

bloomberg.com 07 14 2023