W. Schreiner Parker, Rystad Energy

OSLO

EnergiesNet.com 11 30 2023

| A note from our Senior Vice President and Head of Latin America, W. Schreiner Parker Javier Milei has won the presidential election in Argentina and will steer the battered country for at least the next four years. His previous victory in the PASO primaries foreshadowed the results somewhat, but the actual outcome was far from guaranteed. Sergio Massa, the super minister of economy for the Peronist Frente de Todos party, had seen a late surge in popularity after winning the first-round ballot but couldn’t convert when faced with a runoff scenario with Milei. Since Argentina is suffering from annual inflation in the 140% range and concurrently passing through a currency devaluation, which hasn’t been seen in Latin America outside of Venezuela, it’s probably not a surprise that voters had little trust in Massa’s ability to turn the tide. The fact that he was a candidate for the ruling party didn’t help either, with “anti-incumbentism” reigning supreme on the continent just now. Massa’s proposed playbook was well known to the electorate, whereas Milei’s is still somewhat nebulous, and that fact helped attract voters looking for a change. Apart from Mauricio Macri’s four years in the Casa Rosada and the tumultuous two-year administration of Fernando de la Rua at the beginning of this century, the Argentine people have been under Justicialista Party leadership since Carlos Menem’s election in 1989. The Justicialista Party represents the continuation of the party founded by Juan Peron in 1946. While the definition of Peronism has developed different currents throughout the decades, namely Kirchnerismo, the basic tenants remain the same. Javier Milei ran on a platform of radical opposition to those Peronist pillars but didn’t have to elaborate much more than that. He seized on a wave of popular discontent that has washed over Latin America in the last four years. Except for the Colorado Party in Paraguay, every other country in the region has seen the party holding the presidency ousted at the ballot box in favor of the opposition since 2019. And Argentina proved no different. Now it is time to see what Milei is made of, what can come out of everything that was said on the campaign trail and what will come to fruition. Talk of dollarizing the economy and privatizing state-owned companies like YPF and Aerolineas Argentinas are making big headlines right now. Although Argentine markets were closed on Monday, 20 November, for a federal holiday, YPF shares traded in New York shot up 40% the day after the election. Compared to the stock’s 100-day average of 1.85 million shares, the Monday session saw almost 15 million shares traded. Although those gains were pared back toward the end of the trading day, the stock still finished up 34% from last week. This type of optimism from the market underpins a more broadly pervasive hopefulness than what’s been seen in Argentina for an extended time. The Vaca Muerta shale play is an investment dream from a subsurface perspective but has long been dogged by aboveground risk that has capped its growth potential. Currency controls, protectionism on the manufacturing and technology front and rampant union interventionism have all complicated the picture in what is the world’s most prospective shale play outside of the United States. The feeling is that Milei may be able to radically break the chains that have weighed down investment in the country. But radically breaking anything is also fraught with potential disaster, and any economist worth their salt will say that things must get worse before they get better. The main issues now facing Milei are teamwork and time. Teamwork will be the issue in the Congress. If Milei can secure congressional help from Macri’s Juntos por el Cambio party, or any other party for that matter, to enact his visions, it isn’t clear. Time will be the issue with the electorate. The vast majority of Argentines are living through an economic hurt that hasn’t been felt in a generation, and while they may be up for trying something new, they’ll want to see results quickly. If Milei can’t relieve some of the pressure in the short term, his popular mandate will erode quickly. The country’s problems didn’t manifest overnight, nor will their remedies be effectual at that time. How long will the long-suffering Argentines give Milei before their patience runs up? All the best, Schreiner Parker |

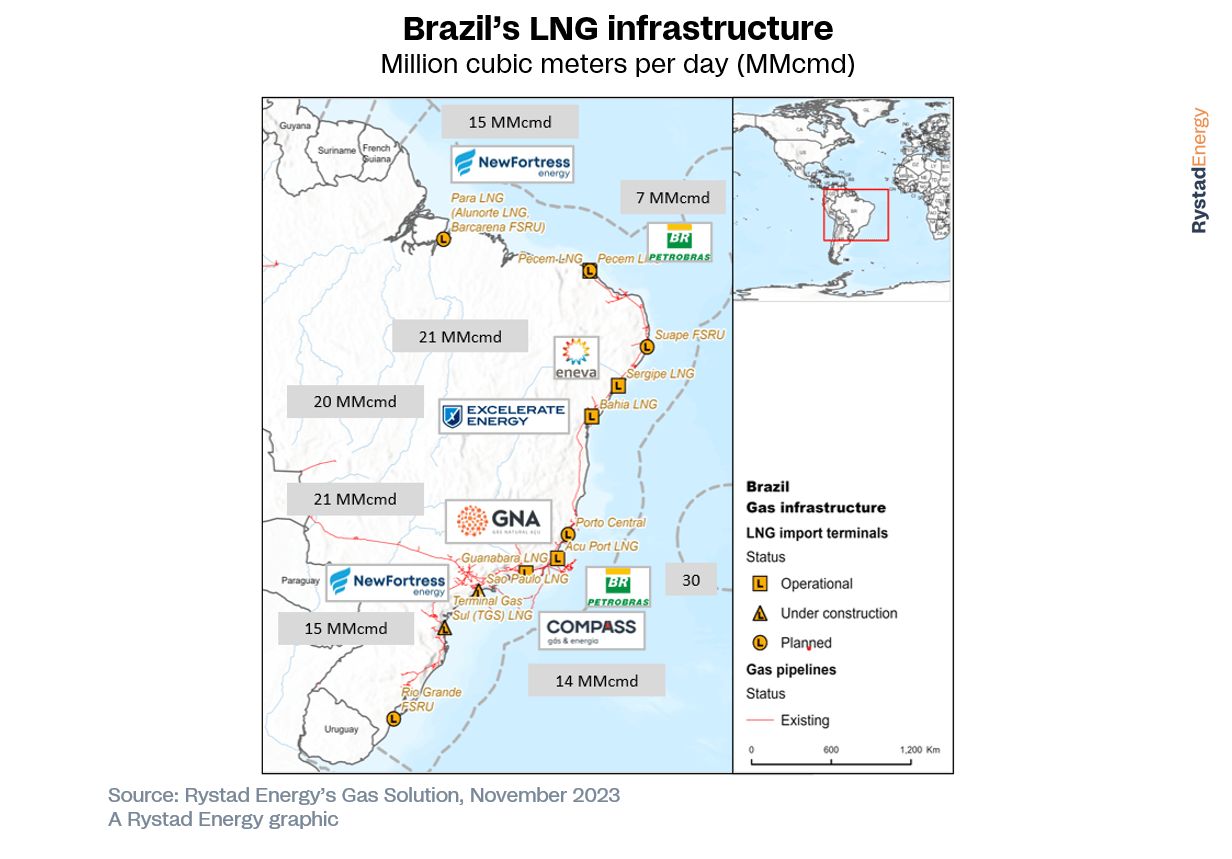

| South America’s gas market: shifting dynamics and network priorities With gas wells drying up in Bolivia, but seemingly endless gas production from Argentina’s Vaca Muerta shale deposit and promising new deepwater reservoirs identified offshore Brazil’s Pre-salt and Equatorian margin, South America is likely to see a reshuffling of gas market dynamics in the coming years. Brazil, Argentina and Bolivia are currently interconnected by a network of gas pipelines which help manage supply and demand balances between the three countries. Argentina and Brazil’s promising new gas resources could see a rejigging of this relationship in the coming years. However, the success of these plans depends on construction of critical gas transportation infrastructure in the years ahead, which could either see the region flooded with gas or choked by bottlenecks. How do we see the dynamics between these countries evolving? We anticipate that Bolivia’s gas production will decline, jeopardizing exports to Brazil and Argentina. By 2032, we believe that Bolivia will become a gas importer, unable to supply even its own domestic demand, requiring gas imports or demand destruction. Bolivian transportation companies are not planning to invest in the grid in the coming years and we foresee an under-utilization of the infrastructure, which may prompt them to seek to connect with Argentina’s gas industry. The key challenge for the next few years will be to maintain operations on the parts of Bolivia’s transportation network that are set to become idle. Our forecast for Brazil gas balance shows that the country is expected to continue importing gas, either from a neighboring country such as Argentina or by importing more gas in the form of LNG. Brazil’s NTS network operator is already planning for additional volumes from pre-salt fields and declining volumes from Bolivia but ignoring for now the possibility of imports from Argentina. TBG shows no clear signs of reversing its pipeline network or reinforcing interconnections to fill the pipelines with pre-salt gas, neither plans to receive Argentine gas. Instead, the company is focusing to solve physical bottlenecks to enable southern demand growth. TAG is focusing efforts to increase northeast flow capacity and will need significant investments in new links to receive a potential 18 MMcmd of gas from Sergipe-Alagoas that is currently planned by Petrobras to start in 2027 but we consider a lower capacity reaching the market. Aside from this, no links are planned in new regions of Brazil such as the countryside with no other construction work being planned or undertaken. For the next few years, despite increased volumes coming from its pre-salt fields, Brazil has concrete plans to reinforce its LNG infrastructure to keep its options open. Argentina’s gas network plans are focused on maximizing the potential of the Neuquen gas resources, which are seen as the future of the nation’s gas supply, helping offset reducing conventional gas production in the south. The intention is to minimize LNG imports although, according to our analysis, after all the infrastructure planned investments Argentina is likely to continue importing LNG during peak winter periods. The reversal of the northern section of the pipeline is a clear sign that Bolivian gas will no longer be needed. The Fénix field, located off the coast of Tierra del Fuego in southern Argentina, will make use of existing infrastructure with no further network investments scheduled for this region. Source: Rystad Energy Brazil Gas Solution |

|

| Colombia eyes offshore resurgence after recent Glaucus gas find Colombia’s upstream sector is expecting a significant boost following the recent Glaucus offshore gas discovery by Shell and Ecopetrol, with other prominent players such as Petrobras and Chevron eyeing increased activity in the country’s waters. The renewed interest in offshore drilling comes at a pivotal time for Colombia’s exploration sector, which faced setbacks earlier this year when the government of President Gustavo Petro decided not to issue new licenses for oil and gas exploration. This strategic shift aligns with the country’s commitment to transition towards a more sustainable economy, emphasizing renewables and tourism. Despite the setback for the upstream sector, there are efforts to revitalize exploration, with state player Ecopetrol exploring the possibility of resuming activities in previously suspended contracts. Following the recent Glaucus find and a strong 2022 for exploration in the country, Rystad Energy assess prospects for Colombia’s exploration sector. Offshore opportunities Following plans outlined by Petrobras, Chevron, Shell and Ecopetrol, next year is poised to be a pivotal one for Colombia’s offshore sector. There are ambitious plans for up to four offshore probes to be drilled, with one recently spud. Notable among the planned wells are two wildcats: Buena Suerte-1 in the Tayrona Block, operated by Petrobras with Ecopetrol as a partner; and Cumbia-1 by Chevron and Shell in Block COL 3. Additionally, two appraisal wells are scheduled to assess the 2022 Uchuva discovery. Ecopetrol has started drilling the Orca Norte-1 probe in the country’s Caribbean waters using the semisubmersible Noble Discoverer. The well is appraising Petrobras’ Orca discovery made in 2014. Ecopetrol now holds control over the Orca gas discovery after Petrobras relinquished part of the Tayrona permit to concentrate on the Uchuva find nearby. A potential obstacle to an otherwise hopeful 2024 is insufficient offshore infrastructure. Even if additional offshore production comes to fruition, logistical challenges remain due to the inadequacy of the existing pipeline network, which will need extension. Colombia’s capacity to transport gas from offshore fields is limited and failure to address this issue could impose constraints on prospective production. Can halt on new license awards be reversed? Colombia relies heavily on revenue from oil and gas production, which makes a crucial contribution to the economy. Currently facing a shortage of proven oil and natural gas reserves, the country’s industry suffered a significant blow during the Covid-19 pandemic due to operational pauses and project delays. From 2019 to 2023, production plummeted by approximately 10%. Compounding this challenge, many potential exploration areas in Colombia are unlikely to be developed. This is attributed to President Petro’s plans to cease awarding new exploration contracts and ban hydraulic fracturing, dissuading potential investors. Some international energy companies are exiting Colombia and Rystad Energy estimates significant decrease in exploration investments compared to the previous year, projecting figures of between $650 million and $700 million. This trend is expected to force Colombia to increasingly rely on its existing, diminishing reserves. With the president aiming to limit oil exploration, we predict a decline in private investment in exploration. Colombia may find itself relying on foreign oil as early as the next decade, making it vulnerable to the volatility of oil prices and diminishing production. The government is striving to revitalize existing oil and gas projects without granting new exploration licenses, with a $38-million initiative, aiming to revive approximately 20 suspended oil and gas contracts, as outlined by the National Hydrocarbons Agency (ANH). While President Petro is discouraging new exploration, he has been encouraging energy companies to develop already awarded blocks. However, the oil industry has been advocating for new licensing rounds to tap into Colombia’s areas of significant potential. Colombia is experiencing substantial supply-side challenges in the production of domestic natural gas. The consumption of this fossil fuel is steadily increasing, surpassing the available supply and creating a significant demand-supply gap. President Petro’s decision to ban new oil and gas licenses in favor of a transition to greener energy sources has raised concerns that Colombia may become reliant on fossil fuel imports as production dramatically decreases over the next decade. To ensure energy security, the president faces the dilemma of either allowing new licensing or rapidly developing the country’s renewable energy sector to bridge the anticipated demand gap in the coming decade. Source: Rystad Energy Upstream Solution |

rystadenergy.com 11 30 2023