The U.S. exploration and production sector has one overriding objective this year: relevance. That might seem odd for an industry that over the past year was the best performer in the stock market by far and that remains the source of America’s two biggest fuels, oil and gas.

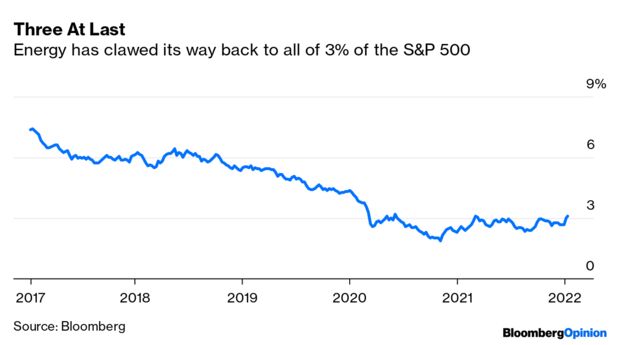

Yet consider. For the past month, oil prices have been on a tear, pulling the sector up with them — so much so that energy stocks now comprise all of … 3% of the S&P 500.

Oil has traded above $80 a barrel three times in the past five years. When that happened back in the fall of 2018, energy was 6% of the S&P 500 (it was 16% when oil hit its all-time peak in 2008). But soon after, the last vestiges of investors’ interest in the sector gave way. Tellingly, when oil prices then fell, stock multiples fell with them, breaking the historical pattern (see this). In essence, the market couldn’t see a way back for E&P companies and walked.

The old inverse relationship between oil prices and multiples has reasserted itself in the past year’s rally. Nature, or natural resources, is healing, as the bulls might say. Still, at 3%, it has a way to go. And higher oil (and gas) prices, while useful pain relief, aren’t the whole cure.

The main deficit is one of trust. Although the gathering, if volatile, pace of decarbonization certainly hangs over long-term valuations, what really haunts E&P is the past. The shale boom of the 2010s was a triumph of market share over market returns, when energy customers benefited from a surge of capital into the product (similar to anyone who took an Uber ride or rented a WeWork office space), but investors did not (see this). Sponsored ContentInnovating the Future of Biodegradable BiomaterialsYokogawa

This deficit is apparent in all manner of comparative data. At 3.8%, energy sports the highest dividend yield of any sector, more than double the index average. At nine times, energy’s multiple of trailing cash flow is the only one in single digits. Perhaps most glaringly of all, energy’s share of the S&P 500’s market cap is the lowest relative to share of projected earnings of any sector.

The message in that discount: Investors don’t trust energy to spend its earnings wisely.

Fortunately for the sector, it has begun rebuilding trust. E&P companies, after many years of habitually spending more cash than they brought in, have become more disciplined. According to the quarterly “State of the Business” roundup by Bob Brackett at Bernstein Research, the sector clocked its fifth consecutive quarter of organic free cash flow (i.e., before acquisitions) in the three months ending September. At almost $15 per barrel of oil equivalent, this was the highest since the third quarter of 2008. The big difference is that, while oil averaged $118 a barrel back in the summer of 2008, it was just $70 in the summer of 2021. Keep in mind that for the last three months of 2021, oil averaged $77.

More of that cash is being either returned to investors or, just as important, used to repair balance sheets: At 61%, energy has the lowest ratio of debt to equity of any sector in the S&P 500. Moreover, while production is expected to rise this year — the U.S. Energy Information Administration just forecast an extra 640,000 barrels a day in 2022 — productivity gains have continued through the pandemic. In October, the industry produced more than 3,300 barrels-equivalent per worker, up from about 2,700 at the start of 2020. Opinion. Data. More Data.Get the most important Bloomberg Opinion pieces in one email.EmailSign UpBloomberg may send me offers and promotions.By submitting my information, I agree to the Privacy Policy and Terms of Service.

All of this tees up a continued rally in a sector enjoying the uncontrollable tailwinds of oil prices and broader inflation. This year, the rally will depend less on the price of a barrel on any given day than on the multiple that investors are willing to ascribe to the profits from that barrel. And that is a function of how well discipline will hold. Managing cash flow rigorously rather than chasing prices mindlessly, in other words, offers the best insurance for E&P stocks against any weakness in the oil market. That will spell the difference between indifference and relevance.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal’s Heard on the Street column and wrote for the Financial Times’ Lex column. He was also an investment banker. Energiesnet.com does not necessarily share these views.

Editor’s Note: This article was originally published by Bloomberg Opinion, on January 11, 2022. All comments posted and published on EnergiesNet.com, do not reflect either for or against the opinion expressed in the comment as an endorsement of EnergiesNet.com or Petroleumworld.

Use Notice: This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in our efforts to advance understanding of issues of environmental and humanitarian significance. We believe this constitutes a ‘fair use’ of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U.S.C. Section 107. For more information go to: http://www.law.cornell.edu/uscode/17/107.shtml.

bloomberg.com 01 12 2022