Production, Institutions, and the Limits of the Oil Rebound

The door is open. The investment has not walked through. (Image:AI)

By Elio Ohep, EnergiesNet

PHOENIX

EnergiesNet.com 05 29 2026

In February 2026, writing in Americas Quarterly, Francisco Monaldi explained clearly why Venezuela’s oil renaissance still faces serious institutional problems. Since then, the noise around Venezuela’s energy sector has only grown louder. Talk of an imminent industry opening — American companies moving in, production targets doubling, a new Hydrocarbons Law unlocking billions — has become common in business and political commentary on both sides of the Atlantic. Yet five months of actual data prove Monaldi was right, and the situation is even more complicated than he described.

Venezuela is in the middle of a political earthquake. The capture of Nicolas Maduro by U.S. forces in January 2026 ended more than two decades of Chavista rule and opened, for the first time in a generation, a real conversation about the country’s future. In oil circles — Houston boardrooms, Wall Street and international trading floors, Washington policy offices — the question is being asked urgently: does this moment finally unlock the investment cycle Venezuela has been waiting for?

The honest answer is: not yet. And understanding why requires carefully separating two very different things that are easy to confuse: a political opening and an institutional transformation. Venezuela has the first. It does not yet have the second. And in the oil business, the second is what brings in capital.

Five months of actual data prove Monaldi was right — and the situation is even more complicated than he described.

A Recovery Built on Old Foundations

What is happening in Venezuela’s energy sector today is not an investment cycle. It is a partial operational recovery, driven almost entirely by companies that were already in the country before the expropriations and institutional collapse of the Chavez-Maduro era. These operators — Chevron, Repsol, Eni, Maurel & Prom — are recovering their own existing assets. They are not making major new long-term bets on Venezuela. The difference is important, and the production data makes it clear.

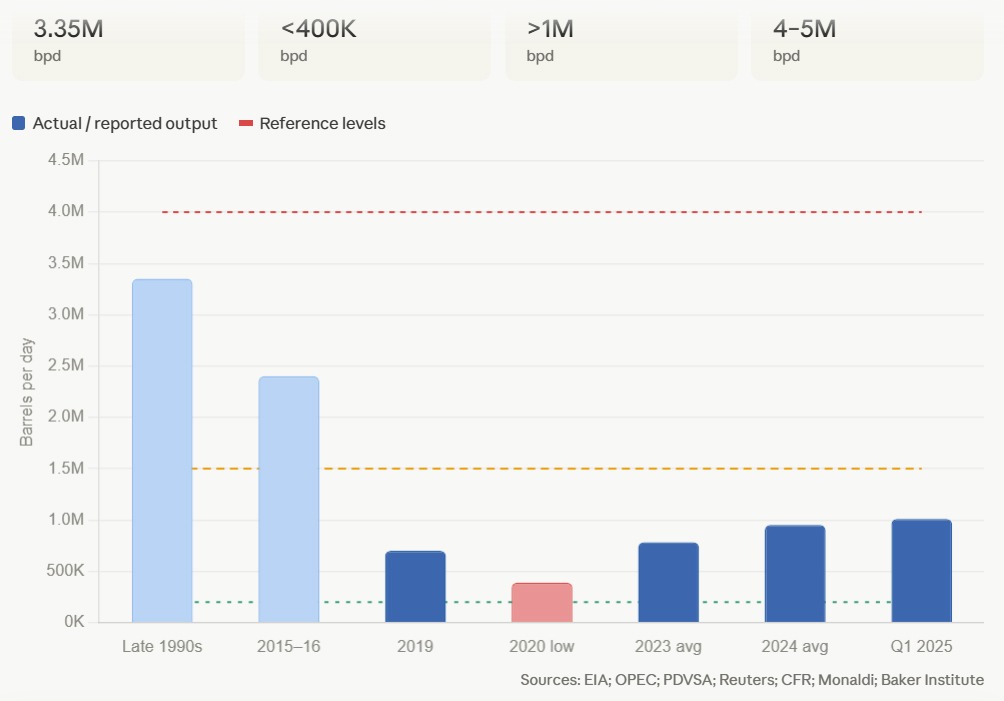

Venezuela produced over 3.2 million barrels per day at its peak in the late 1990s. By 2015-2016, after years of political interference and chronic underinvestment, output had fallen to around 2.3-2.5 million barrels per day. By 2019, the combined effect of poor management, corruption, the mass departure of technical talent, and tighter U.S. sanctions had pushed production to roughly 700,000 barrels per day. In 2020, under maximum-pressure sanctions and the pandemic, Venezuela bottomed out below 400,000 barrels per day — a historic collapse for a country with the world’s largest proven reserves.

The partial easing of sanctions in late 2023 allowed a modest rebound. Production averaged around 952,000 barrels per day in 2024, briefly crossed one million barrels per day in early 2025, and is trending toward 1.2 million barrels per day in May 2026. These are real gains. But they reflect the reactivation of existing fields and facilities, not the arrival of major new capital. Chevron’s joint ventures alone account for roughly 200,000 barrels per day — produced under a specific U.S. government license, not under any open regulatory system designed to attract new entrants. The ceiling for this type of recovery is estimated at around 1.5 million barrels per day. Going beyond it requires new fields, new upgrading infrastructure, and sustained capital commitments measured in tens of billions over a decade or more.

Francisco Monaldi, director of the Latin America Energy Program at Rice University’s Baker Institute, described the scale of that challenge clearly when he wrote in January 2026: “Geology is not Venezuela’s problem. The country possesses vast reserves, faces relatively low geological risks, and enjoys moderate extraction costs. The real obstacles to investment are not found below ground but above it. They are political, regulatory, and institutional in nature. Achieving that outcome [full production recovery] would require more than a decade of consistent effort and investments exceeding $100 billion.”

— Francisco Monaldi, Baker Institute / Substack, January 6, 2026

That capital has not arrived. And the events of January 2026, dramatic as they were politically, have not yet changed that reality. As Monaldi told Bloomberg in January 2026, rebuilding Venezuelan output to its historical peak would require companies to invest about $10 billion per year over the next decade — equal to more than a third of ExxonMobil’s entire global annual capital spending budget.

What the Market Said When It Mattered

The clearest test of investor confidence came in the days immediately following Maduro’s capture. President Trump met with oil executives at the White House on January 9, 2026, calling on them to move quickly into Venezuela and promising that their investments would be safe. He spoke of $100 billion in investments. Markets briefly surged. Then reality returned.

Politico’s headline captured the outcome clearly: “Uninvestable: Trump pitch to oil executives yields no promises.” The companies Trump was counting on did not commit. The word “uninvestable” was not Politico’s description — it was Darren Woods’, CEO of ExxonMobil, speaking at that same White House meeting, as reported by Fortune, the Washington Post, CNBC, and Axios:

“If we look at the commercial constructs and frameworks in place today in Venezuela — today, it’s uninvestable. Significant changes have to be made to those commercial frameworks, the legal system. There has to be durable investment protections. We’ve had our assets seized there twice, and so you can imagine to re-enter a third time would require some pretty significant changes from what we’ve historically seen here.”

— Darren Woods, CEO, ExxonMobil, White House, January 9, 2026, as reported by Fortune and CNBC

Ryan Lance, CEO of ConocoPhillips, was equally cautious. As reported by CNBC at the same White House meeting, Lance called for the restructuring of PDVSA and said the banking sector would need to help restructure Venezuela’s debt and provide billions in financing before ConocoPhillips could make any long-term commitments. Venezuela’s energy system, he said, needs to be “restructured” before new investment can be considered.

The gap between political enthusiasm and corporate caution was not accidental. It reflected a realistic reading of conditions on the ground. Monaldi explained the situation clearly in an interview with Marketplace/NPR on April 16, 2026:

“Chevron produces 25% of Venezuela’s oil. Also, they are an incumbent company. They are just expanding their footprint. There are a couple of other companies that have a similar situation. But the rest are companies that would have to figure out how to go back to the country to sign new deals — and I think that will take some time to figure out the details for these companies to really make significant investments in the country. Venezuela is so far adding very little additional barrels to the world market.”

— Francisco Monaldi, Marketplace/NPR, April 16, 2026

David Voght, Managing Director of IPD Latin America, has described the current situation with similar clarity, noting in industry publications that Venezuela’s oil sector is operating in a holding pattern — companies maintaining what they already have rather than expanding, while waiting for more clarity on the institutional and regulatory framework.

The Problem Is Not the Law

On January 29, 2026, Venezuela’s National Assembly passed the most important reform to its hydrocarbons framework since the sector was nationalized in 1976. The amended Organic Hydrocarbons Law opens paths for direct private participation in upstream activities, lowers royalty burdens, introduces new contractual structures, and expands access to international arbitration for dispute resolution. On February 13, OFAC issued General License No. 49, authorizing U.S. individuals and companies to engage in new investments in Venezuelan oil and gas, including the formation of new joint ventures. Taken together, these are meaningful steps. For the first time in decades, the legal structure is moving in the right direction.

PDVSA CEO Hector Obregon acknowledged as much in January 2026, as reported by AFP: “We had a law that was not up to date with what we needed as an industry.” Obregon set a target of growing production by at least 18 percent in 2026 from a base of approximately one million barrels per day — an ambition that reflects real intent, but one the industry has received cautiously.

The reason for that caution has been explained repeatedly by those who know the sector best: the problem was never just the wording of the law. It was always the lack of institutions capable of enforcing it.

Ricardo Hausmann, professor at Harvard’s Kennedy School and former Venezuelan minister of planning, put it directly in Fortune in January 2026:

“These are self-inflicted wounds. If you want to recover oil, you need to go back to rule of law.”

— Ricardo Hausmann, Fortune, January 9, 2026

Hausmann further argued in Project Syndicate in February 2026 that Trump’s plan to prioritize oil reconstruction before elections is misguided — that democratic legitimacy is a requirement, not something that comes later, for sustainable investment recovery. At Davos in January 2026, as reported by the World Economic Forum, he warned that what is being described as “stability” in Venezuela may prove temporary for long-term prospects without a genuine democratic transition and restoration of rights.

Elisabeth Eljuri, energy lawyer and independent arbitrator with decades of experience in Venezuelan oil and gas, explained the two requirements especially clearly in a widely circulated LinkedIn post in January 2026:

“First, the rule of law required for those massive investments into Venezuela to actually take place within a reasonable period of time. This means a proper constitutional, legal and treaty framework needs to be in place. This will take time. It will not happen overnight. Some treaties have been terminated, suspended or are soon to expire. The Hydrocarbons Law by design does not work. It is not consistent with the way the E&P industry operates around the world or in those oil jurisdictions that will be competing with Venezuela for the same capital. Existing investments must be respected, which is usually handled with grandfathering provisions.”

— Elisabeth Eljuri, LinkedIn, January 2026

On the contractual framework, Eljuri was equally specific:

“Second, another critical piece of this will be a new contractual framework that will allow the proper balance between investors — the capital and technology providers — and the State as the resource owner. Petroleum economics will play a key role to ensure that the new framework is durable and will survive over time and through oil price fluctuations. That framework should also reflect the normal forms of E&P investment structures used around the world to develop a top-level upstream oil business. This is not a ‘copy and paste’ exercise by anyone with a law or geology degree.”

— Elisabeth Eljuri, LinkedIn, January 2026

Luis A. Pacheco has reinforced this point, emphasizing that Venezuela needs not only a modern Hydrocarbons Law but also independent regulators and a framework respected across future governments. Luis Giusti, former president of PDVSA and one of the architects of Venezuela’s 1990s oil opening, has argued in industry forums that the experience of that period showed what is possible when contracts are credible and regulators are independent — but that what Venezuela needs now is a completely new institutional structure, not cosmetic reforms. Ali Moshiri, former president of Chevron Africa and Latin America, has also noted that no company will commit billions without predictable and enforceable rules governing the operating environment.

FTI Consulting, in a detailed sector assessment published in early 2026, pointed to a clear gap between U.S. government ambitions and the actual position of oil companies: while Washington has presented Venezuelan oil as a strategic asset ready for quick reintegration into Western markets, the industry has responded cautiously, citing concerns about legal durability, political stability, and the risk of recovering capital in an environment without proven institutional continuity.

The China and Russia Question: A Complication the Optimists Ignore

Any serious analysis of Venezuela’s oil sector must address a dimension that is often minimized in Washington-centered discussions: the deeply established positions of Chinese and Russian national oil companies, which together account for roughly 20 percent of current Venezuelan production — and which represent one of the most difficult obstacles to any real industry opening.

CNPC and CNOOC — China’s two main state oil companies — hold stakes in several joint ventures with PDVSA, especially in the Junin heavy oil blocks in the Orinoco Belt. China is also Venezuela’s largest bilateral creditor, with estimates of outstanding loans ranging from $10 billion to $20 billion, much of it backed by future oil deliveries. These oil-for-loan agreements have meant that a significant share of Venezuelan crude output goes to China at below-market prices to service debt — a structural burden on the sector’s finances that any future government will eventually have to confront directly and publicly, at real diplomatic cost.

Rosneft’s position is even more complicated. Russia’s state oil company had major operations in Venezuela before 2020, when U.S. secondary sanctions forced it to transfer its assets to a Kremlin-controlled entity — Roszarubezhneft — specifically created to hold the Venezuelan portfolio outside the reach of OFAC enforcement. Those assets, representing roughly 10 percent of production, remain in legal and operational limbo. A future Venezuelan government trying to normalize relations with the United States will likely face pressure to unwind Russian involvement; doing so without triggering compensation claims and major diplomatic friction will require careful planning that no transition government has yet fully mapped out.

For the American and European companies that appear in optimistic scenarios about Venezuela’s reopening, the Chinese and Russian positions create a specific problem: any development of the Orinoco Belt — where the country’s largest reserves are located — requires negotiating around existing joint venture structures designed for a different political period. New companies cannot simply bid on acreage. They must navigate a landscape of existing claims, debt obligations, and geopolitical relationships that no new Hydrocarbons Law by itself can resolve. This is the dimension the optimists consistently leave out.

The Weight of the Past

Adding to the challenge is the enormous volume of unresolved legal claims against Venezuela — a direct and concrete legacy of the Chavez-era expropriations that no new Hydrocarbons Law can eliminate overnight. As Kelly B. Rose, Senior Vice President and General Counsel of ConocoPhillips, stated when the original ICSID tribunal ruled in 2019: “We welcome the ICSID tribunal’s decision, which upholds the principle that governments cannot unlawfully expropriate private investments without paying compensation.”

That principle, confirmed in 2019, was reaffirmed in January 2025 when ICSID’s annulment committee upheld ConocoPhillips’ award in full. With accumulated interest accrued through 2026, the total now exceeds $11 billion — up from the original $8.7 billion award confirmed by ICSID in January 2025. ExxonMobil holds a separate billion-dollar award. Total international arbitration claims against Venezuela exceed $60 billion. Citgo — Venezuela’s most valuable foreign asset and its main footprint in U.S. refining — is now the subject of competing creditor actions, with a single claimant’s $7.38 billion bid already recommended by the court-appointed auctioneer.

Any serious investor evaluating Venezuela must weigh not only future legal risk, but also the unresolved liabilities of the past — liabilities that Venezuela refused to honor for years and that continue to cloud its relationship with the international capital markets it now urgently needs. Until a credible mechanism is established to address this problem — what some analysts have called a “bad bank / good bank” framework for legacy claims — it will remain a shadow over every new negotiation.

The Untapped Gas Dimension

A complete picture of Venezuela’s energy potential requires recognizing the offshore gas sector — an area almost entirely absent from current investment discussions but one that may eventually prove just as important as the oil recovery debate.

Venezuela holds the largest proven natural gas reserves in Latin America and among the largest in the Western Hemisphere, with estimates exceeding 200 trillion cubic feet. Most are located offshore in the Gulf of Venezuela and the Caribbean — geologically promising areas that have seen almost no commercial development. The Dragon field, located along the maritime boundary with Trinidad and Tobago, has been the subject of intermittent negotiations for years; a framework agreement reached in 2022 has still not produced meaningful progress.

The global LNG market’s tightness — driven by European demand shifts after Russia’s invasion of Ukraine — has created an opportunity for new Atlantic Basin supply that Venezuela’s offshore reserves could theoretically help meet. But the same institutional barriers limiting oil investment apply equally to gas. LNG infrastructure requires longer investment horizons and larger upfront capital than oil, making institutional credibility even more important. A serious post-transition energy strategy for Venezuela would treat offshore gas development as a parallel opportunity — not something that comes after oil recovery, but a separate strategic track requiring its own regulatory framework, partner negotiations, and solutions to the sovereignty questions complicating joint development with neighboring states. That conversation has not yet begun in any serious way.

What a Genuine Recovery Actually Requires

Oil investment operates on timelines of twenty to thirty years. A company committing billions to new Venezuelan upstream projects today is not just betting on the Delcy Rodriguez interim government, or on whatever government follows it. It is betting on the regulatory environment that will exist under future administrations not yet in power. That requires proven institutional continuity — not simply as a promise, but as a track record.

Jose Toro Hardy, Venezuelan economist and former PDVSA board member, has repeatedly emphasized in Venezuelan and Latin American business media that rebuilding investor confidence will require years of consistent policy — not months — and that the sector’s institutional memory of past reversals remains the central obstacle. That memory is long. As Monaldi wrote in Americas Quarterly in February 2026, Venezuela’s past quarter century has been marked by the state repeatedly breaking agreements with foreign investors — a pattern no single law or political transition can erase overnight.

International experience is useful, and not especially encouraging. Post-Gaddafi Libya saw an initial production rebound followed by a prolonged collapse, mainly because political instability made investors unwilling to commit capital at scale. Iraq’s reconstruction attracted major international interest but took nearly a decade to establish anything close to a functioning regulatory environment. Angola’s reform period — a more optimistic example — still required years of consistent policy before major companies committed seriously.

Venezuela’s transition is still in its earliest stages. The opposition coalition led by Maria Corina Machado, which won the 2024 election, has a detailed plan for natural resource recovery but has not yet assumed power. The interim government controls the legislative agenda but operates under heavy external pressure and deep internal uncertainty. The shape of the government that will eventually govern Venezuela — and whether it will have the legitimacy, institutional capacity, and long-term political will to rebuild an independent judiciary and a credible regulatory framework — remains an open question.

Analysts estimate that reactivating existing assets to the 1.5 million barrels per day range will require several years and billions of dollars from incumbent operators. Reaching 2 million barrels per day — the threshold at which Venezuela again becomes meaningfully relevant in global supply terms — would require more than $100 billion in new investment over a decade. That level of capital will not come from legacy operators simply expanding existing operations. It requires genuinely new entrants, making genuinely new commitments, based on genuinely credible institutions — and on a framework that ensures Venezuelans themselves receive fair and lasting value from their resources, not simply another generation of extraction without accountability.

The Door Is Open. The Investment Has Not Walked Through.

Venezuela is not experiencing a new investment cycle. It is experiencing a partial recovery by companies that survived the Chavez-Maduro years and are cautiously expanding operations they never fully abandoned. When Monaldi wrote in Americas Quarterly in February 2026 that the obstacles to Venezuela’s oil recovery are neither technical nor geological but political and institutional, he was correct. Five months later, with the discussion about an imminent industry opening louder than ever, the data confirm his conclusion — and add three dimensions that make the road to a real recovery even longer than he originally described: the Chinese and Russian entanglements that any reopening must deal with; the legal burden of more than $60 billion in arbitration claims that must be resolved before major new capital arrives; and an offshore gas opportunity that no serious post-transition energy strategy can afford to ignore.

The political changes of January 2026 are real and important. They opened a door that has been closed for twenty years. But opening a door is not the same as walking through it, and the global energy industry — which has a long memory and a precise understanding of risk — knows the difference.

The arrival of new capital, new long-term projects, and new global players in Venezuelan energy will only be possible when Venezuela finally has what it has lacked for decades: an independent judiciary, autonomous regulators, a proven commitment to honoring contracts across different governments, and a credible path to resolving the legal and financial legacy of the expropriation era. Only a democratically legitimate government — one with both the mandate and the capacity to build institutions, not simply pass laws — can create the conditions serious investors require, while ensuring that Venezuelans themselves receive fair and lasting value from their resources.

That government does not yet exist. Until it does, Venezuela’s extraordinary resource potential — in oil, gas, and the offshore frontier that remains almost entirely untouched — will remain exactly what it has been for the past twenty years: potential.

Elio Ohep is the Editor of EnergiesNet (former Petroleumworld) and an energy analyst specializing in Latin American oil and gas markets.

EnergiesNet.com 05 29 2026

A note

Where quotes are drawn from press conferences, public forums, or interviews reported by multiple news agencies, the standard journalistic convention applies: “as reported by ……” or “according to outlet………” This is used throughout this story where a direct transcript is not available but the substance has been confirmed by credible reporting.

—

Key quotes

—

DARREN WOODS — CEO, ExxonMobil

White House meeting, January 9, 2026 — reported by Fortune, Washington Post, CNBC, and Axios.

“If we look at the commercial constructs and frameworks in place today in Venezuela — today, it’s uninvestable.”

“Significant changes have to be made to those commercial frameworks, the legal system. There has to be durable investment protections.”

“We’ve had our assets seized there twice, and so you can imagine to re-enter a third time would require some pretty significant changes from what we’ve historically seen here.”

These quotes are confirmed across four major outlets covering the same White House meeting. Use as direct quotes with attribution: “Darren Woods, CEO of ExxonMobil, said at the White House on January 9, 2026, as reported by Fortune and CNBC.”

—

RYAN LANCE — CEO, ConocoPhillips

White House meeting, January 9, 2026 — as reported by CNBC and Fortune.

Called for the restructuring of PDVSA and said the banking sector would need to help restructure Venezuela’s debt and provide billions in financing before ConocoPhillips could make any long-term commitments to re-enter Venezuela.

Said Venezuela’s energy system needs to be “restructured” before new investment can be considered.

Attribution: “Ryan Lance, CEO of ConocoPhillips, said at the White House on January 9, 2026, as reported by CNBC.”

—

FRANCISCO MONALDI — Director, Latin America Energy Program, Rice University’s Baker Institute

Baker Institute / Substack, January 6, 2026 — direct publication.

“Geology is not Venezuela’s problem. The country possesses vast reserves, faces relatively low geological risks, and enjoys moderate extraction costs. The real obstacles to investment are not found below ground but above it. They are political, regulatory, and institutional in nature.”

“Over the past quarter century of chavismo in power, the Venezuelan state has repeatedly reneged on its agreements with foreign investors.”

“Achieving that outcome [full production recovery] would require more than a decade of consistent effort and investments exceeding $100 billion.”

“Under an appropriate contractual and tax regime, oil production would be profitable even at prices as low as $25–30 per barrel. The real obstacles to investment are not found below ground but above it.”

These are from Monaldi’s own published piece. Use as direct quotes: “Francisco Monaldi, director of the Latin America Energy Program at Rice University’s Baker Institute, wrote in January 2026…”

Marketplace / NPR, April 16, 2026 — interviewed directly.

“Chevron produces 25% of Venezuela’s oil. Also, they are an incumbent company. They are just expanding their footprint. There are a couple of other companies that have a similar situation. But the rest are companies that would have to figure out how to go back to the country to sign new deals — and I think that will take some time to figure out the details for these companies to really make significant investments in the country.”

“Venezuela is so far adding very little additional barrels to the world market.”

Attribution: Direct interview, Marketplace/NPR, April 16, 2026.

Bloomberg, January 5, 2026 — as reported by Bloomberg / Yahoo Finance

Rebuilding Venezuelan output to its historical peak would require companies to invest about $10 billion per year over the next decade — equivalent to more than a third of ExxonMobil’s entire global annual capital expenditure budget.*

Attribution: “Francisco Monaldi told Bloomberg in January 2026…”

—

RICARDO HAUSMANN — Rafik Hariri Professor, Harvard Kennedy School; former Venezuelan Minister of Planning.

Fortune, January 9, 2026 — as reported

“These are self-inflicted wounds. If you want to recover oil, you need to go back to rule of law.”

Attribution: “Ricardo Hausmann, professor at Harvard’s Kennedy School and former Venezuelan minister of planning, told Fortune in January 2026…”

Project Syndicate, February 2026 — direct publication

Argued that Trump’s plan to prioritize oil reconstruction before elections is misguided, and that democratic legitimacy is a prerequisite — not a sequel — to sustainable investment recovery.

Attribution: “Hausmann wrote in Project Syndicate in February 2026 that…”

World Economic Forum / Davos, January 2026 — as reported by the World Economic Forum.

Argued that what is being framed as “stability” in Venezuela may prove illusory for long-term prospects without a genuine democratic transition and restoration of rights.

Attribution: “Hausmann argued at Davos in January 2026, as reported by the World Economic Forum, that…”

—

ALI MOSHIRI — Former President, Chevron Africa and Latin America, President of Amos Global Energy Investment. As reported by industry and energy media.

Noted that Venezuela’s resource potential is extraordinary, but that no company will commit billions without predictable, enforceable rules governing the operating environment.

—

LUIS GIUSTI — Former President, PDVSA; architect of Venezuela’s 1990s oil opening

As reported by industry forums and Latin American energy media.

Argued that Venezuela needs a new institutional architecture — not cosmetic reforms — and that the experience of the 1990s oil opening shows what is possible when contracts are credible and regulators are independent.

—

JOSÉ TORO HARDY — Venezuelan economist and former PDVSA board member.

As reported by Venezuelan and Latin American business media.

Has repeatedly emphasized that rebuilding investor confidence will require years of consistent policy — not months — and that the sector’s institutional memory of past reversals remains the central obstacle.

—

DAVID VOGHT — Managing Director, IPD Latin America

As reported by energy industry publications.

Has observed that Venezuela’s oil sector is operating in a holding pattern, with operators maintaining what they have rather than expanding, pending clarity on the institutional and regulatory framework.

—

PDVSA / HECTOR OBREGON — CEO, PDVSA

AFP / Malaymail, January 25, 2026 — as reported.

“We had a law… that was not up to date with what we needed as an industry.”

Set a target of growing production by at least 18 percent in 2026, from a base of approximately one million barrels per day.

*Attribution: “PDVSA CEO Hector Obregon said in January 2026, as reported by AFP”.

—

KELLY B. ROSE — Senior VP and General Counsel, ConocoPhillips

ConocoPhillips official press release, March 8, 2019

“We welcome the ICSID tribunal’s decision, which upholds the principle that governments cannot unlawfully expropriate private investments without paying compensation.”\\

FULL SOURCES LIST

Primary News Sources

- CNBC — “What the Big Oil executives told Trump about investing in Venezuela,” Jan. 10, 2026. https://www.cnbc.com/2026/01/10/what-the-big-oil-executives-told-trump-about-investing-in-venezuela.html

- CNBC — “Maduro overthrow could help these U.S. oil companies recover assets seized by Venezuela,” Jan. 5, 2026. https://www.cnbc.com/2026/01/05/maduro-overthrow-could-pave-the-way-for-us-oil-companies-to-recover-venezuela-assets.html

- Washington Post— “Exxon CEO calls Venezuela ‘uninvestable’ without major reforms,” Jan. 9, 2026. https://www.washingtonpost.com/business/2026/01/09/trump-oil-executives-venezuela-exxon/

- Fortune — “Trump pushes for $100 billion in oil investments in Venezuela while Exxon and others say it’s currently ‘uninvestable,'” Jan. 9, 2026. https://fortune.com/2026/01/09/trump-oil-venezuela-100-billion-exxon-uninvestable

- Fortune — “Trump threatens to keep ‘too cute’ Exxon out of Venezuela,” Jan. 12, 2026. https://fortune.com/2026/01/12/trump-threatens-keep-too-cute-exxon-out-of-venezuela

- Fortune — “Harvard economist Ricardo Hausmann warns against Trump’s profit motive in rebuilding Venezuela,” Jan. 9, 2026. https://fortune.com/2026/01/09/harvard-economist-ricardo-hausmann-venezuela-trump-profit-motive-corruption/

- Axios — “U.S. oil giants tell Trump they’re noncommittal on Venezuela,” Jan. 10, 2026. https://www.axios.com/2026/01/09/us-oil-giants-noncommittal-on-venezuela

- Reuters — “Venezuela’s PDVSA oil sales abroad hit $17.5 billion in 2024 as exports jump,” 2025.

- Bloomberg / Yahoo Finance — “Trump’s Venezuela Oil Revival Plan Is a $100 Billion Gamble,” Jan. 5, 2026. https://finance.yahoo.com/news/trump-venezuela-oil-revival-plan-002532814.html

- Marketplace / NPR — “How Venezuela’s oil industry has changed since Maduro’s capture,” Apr. 16, 2026. https://www.marketplace.org/story/2026/04/16/how-venezuelas-oil-industry-has-changed-since-maduros-capture

- AFP / Malaymail — “Venezuela eyes 18pc oil boost with reforms opening sector to private investors,” Jan. 25, 2026. https://www.malaymail.com/news/money/2026/01/25/venezuela-eyes-18pc-oil-boost

- Al Jazeera — “Oil and US oversight: How is Venezuela’s interim government surviving?” Feb. 6, 2026. https://www.aljazeera.com/economy/2026/2/6/oil-and-us-oversight-how-is-venezuelas-interim-government-surviving

- Time — “What’s Happening With the U.S. and Venezuela, Explained,” Jan. 12, 2026. https://time.com/7344628/us-venezuela-trump-maduro-oil-drugs-war-explainer-questions-answered/

- CBS News — “Venezuela oil industry too shaky for U.S. companies to rush to re-enter,” Jan. 2026. https://www.cbsnews.com/amp/news/venezuela-oil-maduro-chevron-exxon-mobil-conocophillips

- Argus Media — “Venezuela loses appeal of $8.5bn ConocoPhillips award,” Jan. 23, 2025. https://www.argusmedia.com/en/news-and-insights/latest-market-news/2650418-venezuela-loses-appeal-of-8.5bn-conocophillips-award

- Venezuelanalysis — “Venezuela Loses Multi-Billion Dollar ConocoPhillips ICSID Appeal,” Jan. 27, 2025. https://venezuelanalysis.com/news/venezuela-loses-multi-billion-dollar-conocophillips-icsid-appeal/

- Offshore Energy— “Nearly $9 billion win for ConocoPhillips as Venezuela loses arbitration case,” Jan. 2025. https://www.offshore-energy.biz/nearly-9-billion-win-for-conocophillips-as-venezuela-loses-arbitration-case-over-three-oil-projects/

Policy and Academic Sources

- Francisco Monaldi— “Fixing the Venezuelan oil industry will take time, money, and—most importantly—institutional change,” Baker Institute / Substack, Jan. 6, 2026. https://fmonaldi.substack.com/p/fixing-the-venezuelan-oil-industry

- Monaldi, Hernandez & La Rosa — “The Collapse of the Venezuelan Oil Industry: The Role of Above-Ground Risks Limiting FDI,” Baker Institute, February 2020. https://www.bakerinstitute.org/research/collapse-venezuelan-oil-industry-role-above-ground-risks-limiting-fdi

- Francisco Monaldi, Americas Quarterly — “Without Institutional Change, Venezuela’s Oil Bonanza Remains Unviable,” Feb. 2026. https://www.americasquarterly.org/article/without-institutional-change-venezuelas-oil-bonanza-remains-unviable/

- Ricardo Hausmann, Project Syndicate — “Venezuelan Democracy Needs Action, Not Cheap Talk,” Feb. 2026. https://www.project-syndicate.org/commentary/trump-venezuela-plan-wrongly-puts-oil-before-democracy-by-ricardo-hausmann-2026-02

- Council on Foreign Relations — “Increasing Venezuela’s Oil Output Will Take Several Years—and Billions of Dollars,” Jan. 2026. https://www.cfr.org/expert-brief/increasing-venezuelas-oil-output-will-take-several-years-and-billions-dollars

- Council on Foreign Relations — “Assessing Venezuela’s Future After Nicolás Maduro’s Bold Capture,” Jan. 2026. https://www.cfr.org/expert-brief/assessing-venezuelas-future-after-nicolas-maduros-bold-capture

- CSIS — “Maduro Captured: What Comes Next for Venezuela?” Jan. 2026. https://www.csis.org/analysis/maduro-captured-what-comes-next-venezuela

- International Crisis Group — “Venezuela after Maduro: Transaction or Transition?” Jan. 9, 2026. https://www.crisisgroup.org/latin-america-caribbean/venezuela-united-states/venezuela-after-maduro-transaction-or-transition

- Americas Quarterly — “Venezuela: The Post-Maduro Oil, Gas and Mining Outlook,” Jan. 2026. https://www.americasquarterly.org/article/venezuela-the-post-maduro-oil-gas-and-mining-outlook/

- FTI Consulting — “Venezuela’s Oil Sector Recovery: Navigating the Post-Maduro Investment Landscape,” Mar. 2026. https://www.fticonsulting.com/insights/articles/venezuelas-oil-sector-recovery-navigating-post-maduro-investment-landscape

- World Economic Forum — “What next for Venezuela?” (Davos panel), Jan. 2026. https://www.weforum.org/stories/2026/01/venezuela-what-next/

- Baker Institute — “The New Venezuelan Hydrocarbons Law: Scope, Intent, and Viability” (webinar), Feb. 12, 2026. https://www.bakerinstitute.org/event/new-venezuelan-hydrocarbons-law-scope-intent-and-viability

Legal and Regulatory Sources

- Mayer Brown — “Venezuela Transforms Hydrocarbons Sector with New Hydrocarbons Law Amendment,” Feb. 2026. https://www.mayerbrown.com/en/insights/publications/2026/02/venezuela-transforms-hydrocarbons-sector-with-new-hydrocarbons-law-amendment

- Baker McKenzie — “Venezuela’s Hydrocarbons Law Reform: What Businesses Need to Know,” Mar. 2026. https://www.bakermckenzie.com/en/insight/publications/2026/03/reform-organic-hydrocarbons-law-venezuela

- King & Spalding — “Venezuela Reforms Hydrocarbons Law: A Potential Sea Change for Foreign Investment?” Feb. 2026. https://www.kslaw.com/news-and-insights/venezuela-reforms-hydrocarbons-law-a-potential-sea-change-for-foreign-investment-in-the-oil-sector

- National Law Review — “Venezuela’s New Hydrocarbon Framework: Key Considerations,” Feb. 2026. https://natlawreview.com/article/venezuelas-new-hydrocarbon-framework-key-considerations-energy-financial-and

- KPMG — “Venezuela: Amended hydrocarbons law introduces new tax framework,” Feb. 3, 2026. https://kpmg.com/us/en/taxnewsflash/news/2026/02/venezuela-amended-hydrocarbons-law-tax-framework.html

- ConocoPhillips — “International Arbitration Tribunal Orders Venezuela to Pay ConocoPhillips $8.7 Billion,” press release, Mar. 8, 2019. https://www.conocophillips.com/news-media/story/international-arbitration-tribunal-orders-venezuela-to-pay-conocophillips-8-7-billion-for-unlawful-expropriation-of-company-s-oil-investments/

Data Sources

- U.S. Energy Information Administration (EIA) — “Venezuela’s heavy crude oil output increases are limited following U.S. sanctions relief,” Oct. 23, 2023. https://www.eia.gov/todayinenergy/detail.php?id=60762

- EIA / Statista — Monthly crude oil production data, Venezuela, 2021–2025. https://www.statista.com/statistics/1240421/crude-oil-production-monthly-venezuela/

- PDVSA 2024 Financial and Operational Results — As reported by Reuters: 952,000 bpd average production; $17.52 billion in oil sales abroad.

- iSANS — “303 billion barrels of oil and a harsh reality,” Jan. 2026. https://isans.org/energy-sector/303-billion-barrels-of-oil-and-a-harsh-reality-why-venezuela-is-unlikely-to-flood-the-market-anytime-soon.html