- Zampa says restructuring could generate 50 cents on the dollar

- ‘Venezuela bonds are like an option that never expires’

Nicolle Yapur, Bloomberg News

CARACAS

EnergiesNet.com 12 29 2022

A European distressed-debt trader is raising money to buy defaulted Venezuelan bonds trading below 10 cents on the dollar amid signs of easing tensions between President Nicolas Maduro, the political opposition and the US.

Claudio Zampa, the Switzerland-based founder and manager of Mangart Capital Management Ltd., said his Phoenix Recovery Fund has seen more interest and investment pledges since Venezuelan politicians struck an agreement last month to restart talks aimed at setting conditions for 2024 presidential elections. That led the US to ease some restrictions on Chevron Corp to allow the oil producer to expand its operations in Venezuela.

“We are at the start of a normalization process that will eventually lead to a debt restructuring,” Zampa, whose Phoenix fund is independent from Mangart, said in an interview. “Recovery values are much higher than current prices.”

Zampa, who has been involved in restructurings in Argentina and Mozambique, says that Venezuela bonds could eventually be worth 50 cents. He’s making a long-term bet on the country, wagering it will have to restructure one of the world’s largest piles of defaulted debt at favorable terms.

Bondholders have been in the dark since payments were halted on some $60 billion of debt issued by the government and state oil producer PDVSA in late 2017. US sanctions imposed in 2019 aimed at hampering Maduro’s sources of financing, also placed restrictions on US-based investors trying to trade the debt. While Maduro has repeatedly expressed willingness to engage with creditors, there are few signs that a resolution is around the corner.

Since launching the fund in March, Zampa has seen inflows of about $10 million, enough to accumulate bonds with a face value of roughly $200 million. He’s looking to raise another $40 million.

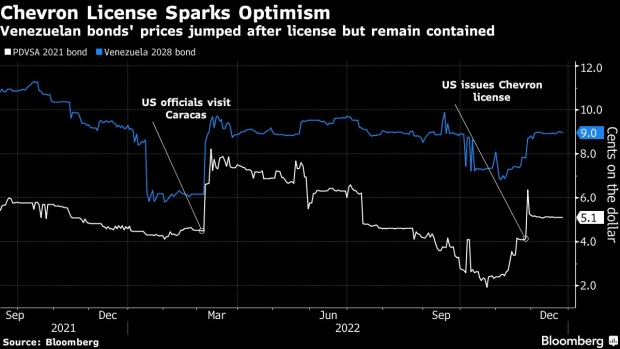

Other funds have taken similar positions, hoping for a big payoff. Just days before the November agreement between Maduro and the opposition, bonds issued by Petroleos de Venezuela SA, known as PDVSA, were trading as low as 2 cents on the dollar. They’re now at 5 cents.

Government bonds also jumped one cent and remain above 9 cents. Uncertainty regarding when and how the US will grant further sanctions relief is preventing prices from rising further since a formal restructuring is nearly impossible under current conditions.

Venezuela’s defaulted debt has accumulated almost $30 billion in interest, according to calculations from EMFI Group Ltd.

The agreement that gave Chevron a six-month license to produce oil in Venezuela and resume exports is a positive development for bondholders as it involves an accord between a US firm and the Venezuelan government that has the blessing of the Biden administration, Zampa said. The deal also allows Chevron to collect on money it’s owed by PDVSA.

The development represents a step forward for creditors, but US bondholders still can’t engage in debt talks with the Maduro administration or enforce their claims in US courts. “Investors are not currently being treated equally,” he said.

Unlike some of its peers, Cayman Islands-based Phoenix is not a litigation fund, Zampa says. It operates separately from Mangart. The fund doesn’t charge management fees, opting instead take a cut of any gains upon redemption.

Zampa emphasizes that investors could still be a long way from seeing a meaningful payout. The next milestone may come with the elections but it could be three more years before any debt talks start, Zampa says. He thinks it’ll be worth the wait.

“Venezuela bonds are like an option that never expires,” he said.

bloomberg.com 12 28 2022