By Nick Butler

OXFORD, England (Project Syndicate)—With images of Russian aggression and war crimes in Ukraine continuing to dominate the media in Europe and around the world, Germany has pledged to cut its imports of Russian gas by two-thirds by 2023. Even more immediately, Robert Habeck, Germany’s vice chancellor and minister for economic affairs and climate action, now talks of the country reducing its Russian oil imports by half by as early as this June.

But cutting imports of Russian natural gas will take longer. The European Union recently created a new agency to buy gas on behalf of all 27 member states. Its first joint purchase, of some 15 billion cubic meters (bcm) this year, will come from the United States in the form of liquefied natural gas. But that is only a beginning.

Europe cannot quickly shift away from Russian gas, particularly in the industrial sector. Russian President Vladimir Putin’s war on Ukraine will prompt intensified efforts to develop more wind farms and solar facilities across the EU. But renewable energy requires specific improvements in infrastructure, which will take time to finance and put in place. Until battery technology allows power to be stored in substantial volumes, Europe will need gas-powered plants for backup energy supply on days without wind or sun.

Supplies already stretched

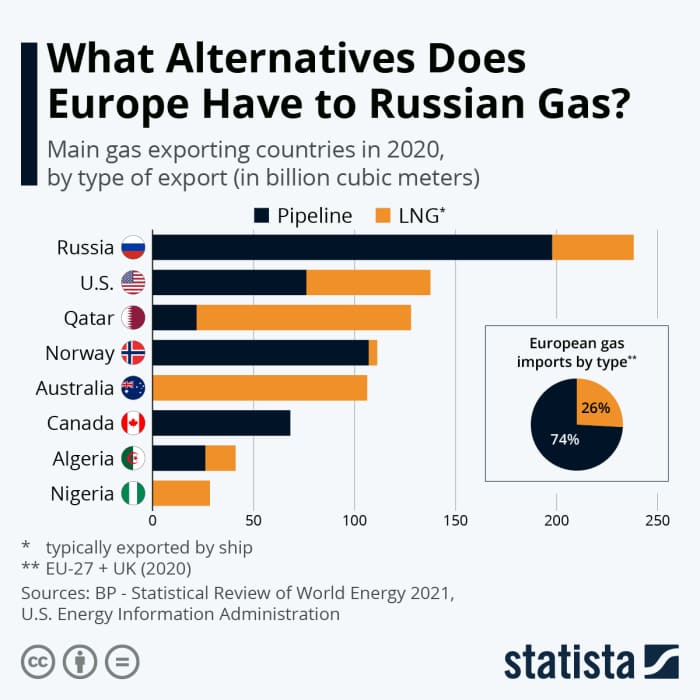

Even with the 15 bcm of LNG from the U.S., Europe will still require another 140 bcm to replace its gas imports from Russia completely. Those supplies will have to come from a world market that was already stretched thin before Russia invaded Ukraine. And European demand for non-Russian natural gas will add to the pressure on prices for countries that depend on imports – not least China, the world’s largest gas importer.

While there is no shortage of gas in the ground, developing these resources and bringing them to market can take three to five years – or more if complex LNG facilities need to be installed. Putin’s war will spur the development of new gas fields, notably in the Middle East and the eastern Mediterranean.

But for the time being, there is only one readily available source of substantial extra supplies: the U.S.

For others, however, the promotion of gas for export represents an unwanted revival of the hydrocarbon-based economy. The gas exported from the U.S. in the form of LNG will generate greenhouse-gas (GHG) emissions, adding to a global total that has already returned to prepandemic levels and is still rising.

Reconcile different views

It is far from clear, however, that the U.S. wants to be the world’s natural-gas supplier of last resort – the Saudi Arabia of the global gas market. For the U.S. oil-and-gas industry and some politicians, gas exports are a rational response to global needs and a welcome new source of revenue and jobs after several lean years. They think a new shale boom beckons, because much of America’s potential gas exports will come as a byproduct of shale-oil developments.

Then there are those who highlight the risk that increased exports will take supplies of gas NG00, +4.63%, and probably of oil CL00, +2.20% as well, out of the U.S. just when consumer prices for all forms of energy are rising rapidly. America has come to enjoy the self-sufficiency in oil and gas that shale has provided, and it is uncertain whether becoming the world’s major gas exporter holds any great attraction.

It will be difficult for President Joe Biden to reconcile these different points of view. His administration’s major legislative initiatives to limit GHG emissions and promote clean energy have stalled in Congress or been reduced in scale and likely impact. The environmental lobby, an important part of the Democratic Party’s voting base, is already expressing disappointment at the lack of progress, amid fears that the Democrats could lose control of Congress in November’s midterm elections.

On the other hand, a large and growing shortage of natural gas in Europe, where there is already talk of rationing, could undermine public support for sanctions against Russia. The temptation for Germany and others to push the Ukrainian government into accepting an unsatisfactory peace deal with Russia will only grow if the impact of gas shortages on the European economy increases.

Putin’s war against Ukraine has put energy security back at the top of the political agenda on both sides of the Atlantic. The choices now facing U.S. and European leaders may be uncomfortable, but they are also urgent and unavoidable.

___________________________________________________

Nick Butler, a visiting professor at King’s College London, is founding chair of the Kings Policy Institute and chair of Promus Associates. Energiesnet.com does not necessarily share these views.

Editor’s Note: This article was originally published by MarketWatch, on April 15, 2022. All comments posted and published on EnergiesNet.com, do not reflect either for or against the opinion expressed in the comment as an endorsement of EnergiesNet.com or Petroleumworld.

Use Notice: This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in our efforts to advance understanding of issues of environmental and humanitarian significance. We believe this constitutes a ‘fair use’ of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U.S.C. Section 107. For more information go to: http://www.law.cornell.edu/uscode/17/107.shtml.

energiesnet 04 18 2022